Credit Card 101 - Master Your Cashflow & Rewards

Master your cash flow and rewards with Credit Card 101—optimise spending and maximise frequent flyer points!

Credit cards are often seen as a taboo topic; more often than not, they are associated with “bad” rather than “good”. While I can see both sides of the coin (or shall we say card?), for me, credit cards and especially credit card rewards have opened up a whole new world of travel possibilities.

As a self-confessed points nerd, I have been obsessed with credit cards for some time now, but there’s always some hesitancy from those not in the know when it comes to using credit for everyday transactions.

I think it all stems from a lack of understanding and some fundamental basics of cash flow management skills. In this post, I want to outline my personal strategies for managing expenses and getting rewarded for doing so.

Cashflow

Let me give you a quick rundown on how I manage my cards to optimise cash flow and get rewarded for every single dollar I spend. It’s actually effortless; I simply avoid cash/debit transactions at all costs. While this might seem simple, it’s actually a crucial step in managing your expenses because, as I always say: a credit card is NOT a loan.

You see, if you spend on credit and only on credit, at the end of the month when the bill is due, you know exactly how much you’re up for. However, if you spend a bit of cash here and there, use your debit card on occasion and use a credit card for a few more purchases… you guessed it: your expenses will look like a mess. Not only that, you might have accidentally spent more than you can afford!

Tip: use credit for all your expenses and leave your money in your savings or offset account where it can work for you. At the end of the billing cycle, use those funds to pay off your balance in full to maximise the value of your reward points.

Unforeseen expenses?

With all that said, credit cards do offer us a lifeline when something unexpected pops up. You know the drill… car breaks down, dentist, taxes and maybe…just maybe you get a call from your local Hermès boutique informing you that your Birkin is finally available for purchase (and yes, it’s an investment).

All those “fun” things life throws our way.

In these instances, one can be “forgiven” to spend a little extra and pay it back at a pace that works for you. American Express has introduced a feature called Plan It Instalments (check out our in-depth guide here). Plan It is precisely for those unexpected expenses, and it’s a way you can manage those without getting charged substantial interest fees.

Plan It allows Amex Credit Card Members to set up payment plans of 3, 6, 9 or 12 months with an up-front low monthly fee to help you manage your cash flow(no need to apply, it’s automatically included). You know exactly how much to pay each month, and plans can be set up in seconds.

Learn more about Amex Plan It here.

How much does it cost to use Plan It?

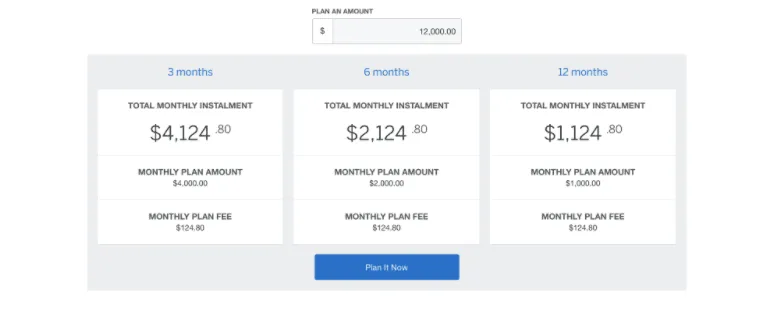

The Amex website has a handy calculator which lets you work out exactly how much you will need to repay and what the fee is for doing so. You can find the calculator here.

For our $12,000 Birkin bag example we would be looking at the following repayment schedule:

Essentially, when used responsibly, Plan It can be a great way to manage your expenses outside of your regular spending habits whether that be for emergencies, retail or travel. Best of all, there’s no impact on your credit score since it’s included with your Amex account.

Side note: New to American Express? Check out our latest sign up bonuses here.

Rewards

If your credit card does not reward you with cash back, frequent flyer miles or rewards points, it should have no place in your wallet. What’s the point of using a credit card if you don’t get anything for it? You might as well use cash or switch to a debit card that lets you earn “some” points or cash back.

Interest Rates Are Irrelevant

Generally speaking, credit cards without a rewards program have a lower interest rate.

On the flip side, rewards credit cards may have a higher interest rate. Does it matter? Not a single bit! I always advocate for paying off the balance on time and in full each month, in which case the interest is 0%. Not only is it 0%, but you would have also earned valuable rewards points, which can then be cashed in for fun things such as travel, gift cards and more.

Summing Up

When used correctly, credit cards (the ones that reward us, the user) can be hugely beneficial. In combination with the right knowledge on how to maximise frequent flyer points, the upside of going completely cashless can be hugely rewarding!

Full disclaimer: this content is sponsored by American Express and does not constitute advice.