13 Tips To Meet Your Credit Card Minimum Spend

Maximise your credit card rewards: 13 savvy tips to easily meet minimum spend requirements.

When it comes to frequent flyer credit cards, the ones that offer the best sign up bonus always come with a “catch”. Well…it’s not really a catch but rather something you need to take into account: the minimum spend.

Ps. make sure to read bonus tip #14 at the end.

All top tier cards which come with a bonus on sign up require a minimum spend. While amounts vary it is unavoidable but at the end of the day, a credit card was designed for spending. That being said, there’s nothing worse than spending money you don’t have, and this is especially true with frequent flyer cards which usually have a high interest rate if you don’t pay off the balance in full each month.

Luckily, most minimum spends are very achievable thanks to this thing called “life” which comes with fun items such as bills, insurance, groceries etc. Necessities to keep us alive can usually be charged to your card so let’s take a look at see how we can optimise our spend in a smart way to meet your new credit card’s minimum spend.

- Supermarket spending: It’s unavoidable for most people so why not optimise your supermarket spending? If you’ve been living under a rock and haven’t heard about cash-back sites such as ShopBack, you’re missing out (ps. sign up via my link and we will both get $10 credit! Sweeeet). ShopBack allows you to purchase Woolworths WISH eGift cards at a 5% discount. These gift cards are digital and can be easily managed through a handy mobile app. You just use them at the checkout to pay; easy. Best of all, these gift cards NEVER expire so you can pre-purchase any amount and quantity you want. Not only will you save 5% on your shopping; it will allow you to pre-pay an essential spend on your credit card.

- Gift Cards: Since we’ve already been talking about gift cards, let’s look into all the other gift cards you can purchase in the supermarket using your WISH eGift cards. Stuff like Netflix, Uber, David Jones, Myer, BWS, Dan Murphys, Big W and certain petrol stations can all be bought in the supermarket with your digital gift cards at 5% off.

- Internet: We all have it (at least if you’re reading this) and it’s something we will keep on paying for. Why not pre-pay it? You can even call up your provider and ask them for a free month or a small discount for doing so. My personal broadband provider Aussie Broadband regularly runs promotions offering 1-2 months free if you pay 1 year in advance.

- Stop paying cash: It goes without saying but ditch your Eftpos card and only keep cash notes for emergencies. There’s nothing worse than mixing cash spend with credit card spend and here’s why: it can mess up your budget and make you overspend + you don’t earn any points by spending cash. For most this is obvious, but I see it a lot; people pulling out their eftpos card or banknotes to pay for something while they have a perfectly good frequent flyer card. By only using credit, it makes it a lot easier to keep track of your spending while keeping your actual cash in either an offset account or a savings account; ready for use when your card bill is due.

- Pre-pay utility bills: Just like your internet bill, there are other unavoidable costs associated with living: water, gas and electricity are the main culprits here, and luckily they can be pre-paid. If you have the budget to do so, pay them in advance and reach your minimum spend without actually spending money on useless shit. Cellphone bills are another easy target on this list.

- Council rates: If you’re a homeowner you’re probably waiting in excitement for your council rates bill to come through each year. NOT! Anyway, since it’s something we all have to deal with eventually; if finances permit, you can simply pay your local council with your credit card even before the bill is issued or due. Minimum spend = done.

- Paying rent: If you’re renting, there are some services out there that allow you to pay your rent via credit card. Unfortunately, there’s a fee attached so you will have to work out if this strategy is worth it for you. Services like RentPay, Rental Rewards and Easyshare are a few you can investigate.

- Travel: If you’re reading this post, chances are you are also into travel. Timing your ticket bookings to coincide with your new credit card will not only help you reach the minimum spend fast, but it could also offer you valuable travel insurance which is a feature of most premium cards. Of course if you’re unsure about travel dates, you can always book a refundable ticket…

- Pay for family and friends: With that, I don’t mean you pay for them, just offer to pay the bill when out for dinner and collect the cash later! You could also add extra supplementary cardholders to your account and allow them to spend (provided they pay you back!).

- Investing: Share trading platform IG Markets allows you to deposit funds using Visa or MasterCard via Paypal. There is a 1% surcharge, but right now they also offer a 10,000 Qantas Points bonus when you place 10 trades. Just avoid opening a CFD account unless you actually know what you’re doing since could stand to lose a lot of money. DYOR! Their ASX share incurs a $10 brokerage fee so keep this in mind as well. You can find out more about this promo here: https://www.ig.com/au/Qantas

- Donate to charity: Feeling generous? Most if not all charities now accept credit cards online, and of course, your donation is tax deductible. On the other hand, if you don’t have the cash to splash around on good causes, take a look at micro lender Kiva. They offer small loans to people in developing countries which you get back at the end of the term. There’s no fee to fund your Kiva account but it is in USD so keep that in mind. Using an FX free card that earns points such as the ANZ Travel Rewards Adventures is ideal.If you don’t want your money tied up for an extended period, look for loan requests which are about to run out of time and clearly won’t meet the minimum asking amount. When you partially fund one of these loans, and the minimum isn’t reached, you get a refund right away.This might look like a dick move because clearly, your intent isn’t to fund anyone’s loan but on the flipside; it’s a morale booster for the person looking to get funding, and it might encourage them to try again after the campaign ends with a better pitch. Big guns like Google are also involved in the contributions on Kiva so if you’re more into charitable organisations that encourage entrepreneurship and where the loan needs to be paid back, Kiva is worth checking out.

- Purchase points/miles: I’m a big fan of strategically purchasing frequent flyer points through programs that allow you to do so. The main ones would be Alaska MileagePlan, American Airlines AAdvantage and Etihad Guest; to name a few. You can check out my guides on this subject and why you should consider it: https://wordpress-320001-1122823.cloudwaysapps.com/category/guides/buying-points/

- Think creative: Whenever there’s money involved, ask yourself: how can I earn points out of this? Most things these days are payable via credit card so next time you have work expenses, put them through your card and ask for a reimbursed or pay your student fees with a card or pre-pay your Spotify account via supermarket gift cards. You can even send money to friends and family via PayPal…sure there’s a fee that doesn’t make it worthwhile long term but to reach the minimum spend required to get a huge sign-up bonus, it could be worth it. The list goes on, so I encourage you to think creatively and before you know it a $7500 minimum spend in 3 months won’t seem that much anymore.

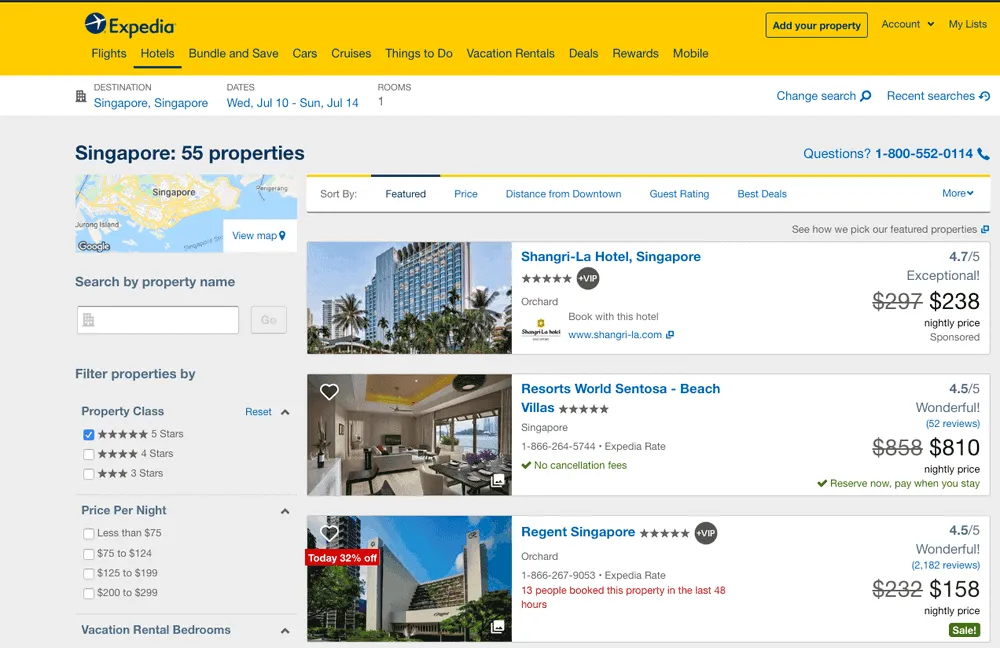

- If you’ve made it this far you deserve a bonus tip! If you’ve ever booked a hotel or a flight you are probably familiar with Expedia. Ever paid attention to booking conditions of hotels? Have a look at the following screenshot and see if you spot it:

Did you see it? That’s right, no cancellation fees.

This doesn’t apply to all hotels but it’s very easy to book a stay 6 months in advance, and take advantage of the “no cancellation fee policy”. It’s an easy way to meet a minimum spend requirement since you can get the charges refunded (if you have to cancel the hotel booking for whatever reason…) after the minimum spend period of 3 months has finished. Of course points from that transaction will be reversed when you get a refund processed on your card but if you keep using your card as per normal, there should be enough points there to compensate for that.